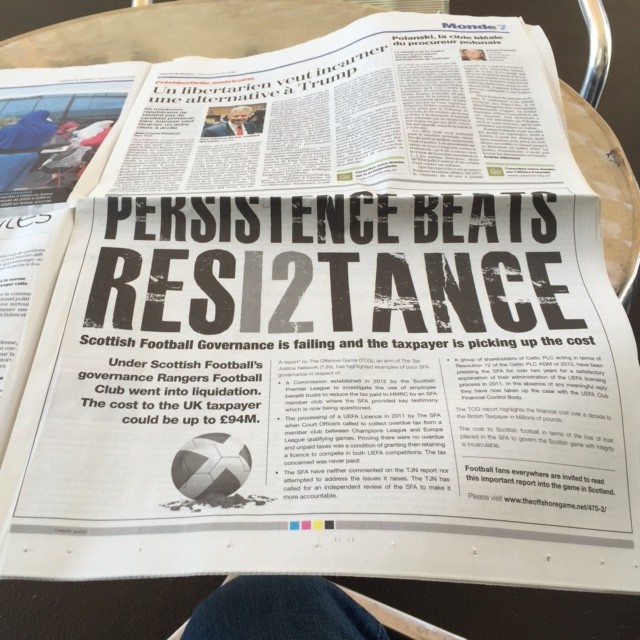

THE Latest Resolution 12, PERSISTENCE BEATS RES12TANCE Update appeared in the 30th Anniversary of the Not The View Celtic Fanzine at the Bayern Munich game on Tuesday evening. Congratulations to the team at NTV on their birthday and for all that they have contributed to Celtic over the years, especially in regard to removing the old board and allowing Celtic to progress to where we are as a club today.

Here is the Res 12 update in full for those of you who didn’t see it in NTV…

PERSISTENCE BEATS RES12TANCE: NOVEMBER UPDATE

Resolution 12 Adjourned at Celtic AGM 2013: A recap and update on where matters now stand.

At the last AGM in 2016 Celtic chairman Ian Bankier stated:

“We continue to meet with shareholders representatives on resolution 12. We understand they have received communication from UEFA on the issue and we will meet with the shareholders next week to understand that communication and how they are moving forward.”

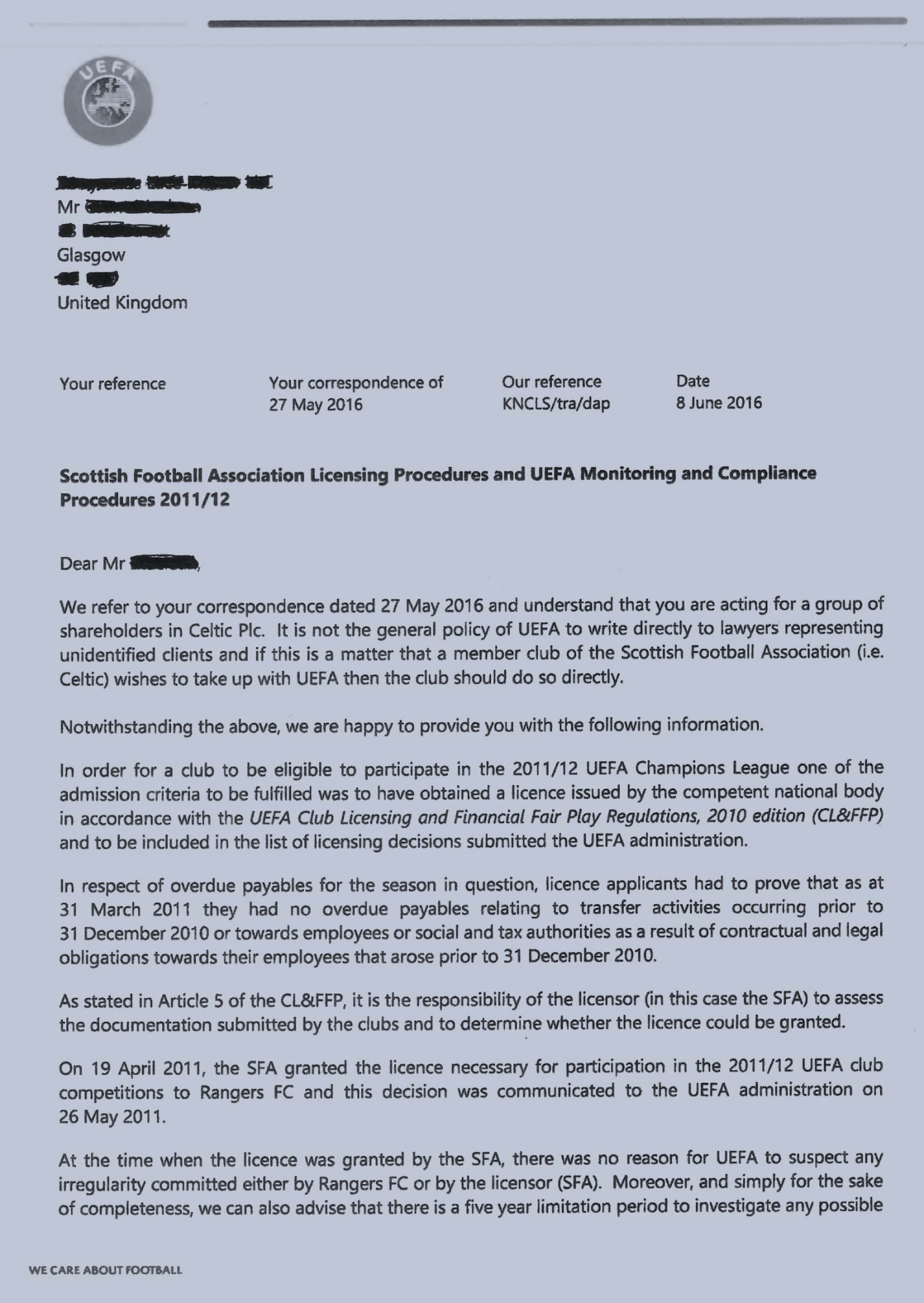

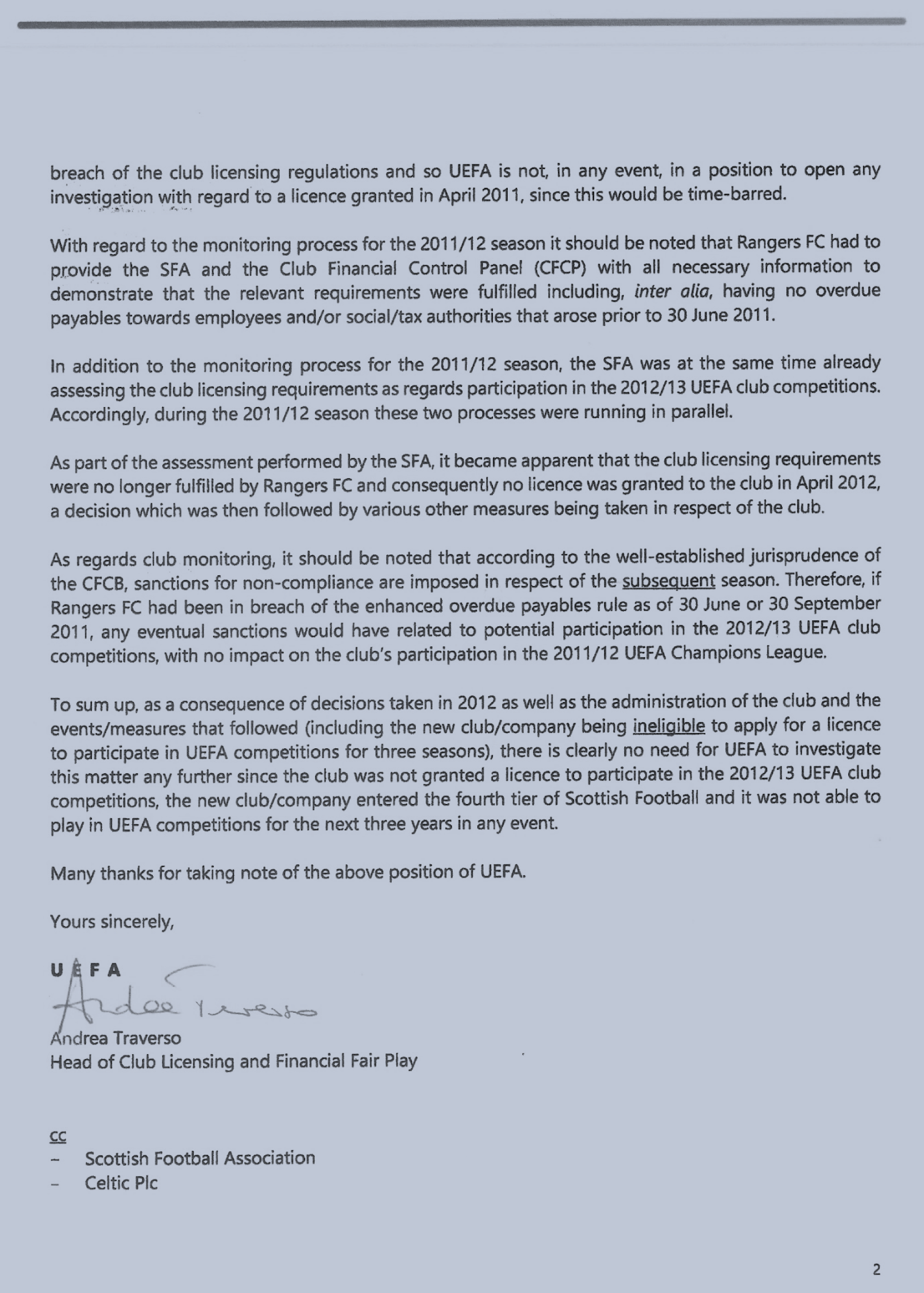

That communication from UEFA is at the end of this article. It not only contains the reasons why UEFA did not wish to progress the matter further, one of which was UEFA considered the current club/company (TRFC/TRIFC) operating from Ibrox to be a new club under Article 12 of UEFA FFP, itself designed to protect the integrity of UEFA competitions, (a concept seemingly alien to the SFA), it also left the door open for Celtic, as a member of the SFA to raise the matter with UEFA if they so wished.

Accordingly Celtic met a shareholders’ representative in the following week to prepare for a full meeting in December 2016.

At that meeting the shareholders’ representatives, having taken the matter as far as UEFA would allow in further correspondence with them at end of September 2016, passed responsibility to pursue the issue with UEFA to Celtic along with all evidence legitimately gathered during 2016.

They also advised Celtic to wait for both the Craig Whyte trial to run its course as well as the final Supreme Court decision on the use of ebts by Rangers FC to pay players for their employment with RFC, both due mid 2017.

Roll on the summer 2017 and the Supreme Court ruled that Rangers had used EBTS in an irregular manner to avoid paying due tax to HMRC, a matter that the SFA wish to draw a curtain over on the basis of not raking over old coals (in spite of those coals still smoldering profusely with the reek of blatant dishonesty, which the SFA were a party to in an attempt to minimize the consequences of more than 10 years cheating by a member club of which the SFA had indications of from 2009 following questions from HMRC.

Significantly in Resolution12 terms, it emerged in the Craig Whyte trial that Rangers had accepted liability on 21St March 2011 with no dispute for the £2.8m tax due from their use of Discount Option Scheme EBTs in 2000/2002. (The wee tax case.)

This acceptance rendered the £2.8m an overdue payable at 31st March 2011 under UEFA FFP Article 50, a status confirmed by the Court of Arbitration for Sport in 2013 when Greek club Giannina FC appealed against a refusal by UEFA to accept their application for a UEFA license in circumstances that very closely mirrored those in March 2011 at RFC including Giannina’s use of private agreements, which UEFA deemed breached fair presentation of their accounts and a reason to refuse a license.

This admission at Craig Whyte trial contrasted with the justification for granting the license quoted by Stewart Regan SFA CEO in a draft he sent for clearance to Andrew Dickson at RFC on 7th December 2011 in which Regan’s justification for granting was a letter from RFC Accountants Grant Thornton dated 30th March 2011.

That letter according to Regan said

“All the recorded payroll taxes at 31 December 2010 have, according to the accounting records of the Club since that date been paid in full by 31 March 2011, between the Club and HM Revenue and Customs in relation to a potential liability of £2.8m associated with contributions between 1999 and 2003 into a discounted option scheme. These amounts have been provided for in full within the interim financial statements.”

Regan then added in his draft (that the SFA never published after discussions, at which both Craig Whyte and Campbell Ogilvie were present in mid December2011):

“Since the potential liability was under discussion by Rangers FC and HM Revenue & Customs as at 31st March 2011, it could not be considered an overdue payable as defined by Article 50. We are satisfied that the evidence from all parties complied with Article 50 and, on that basis, a licence was awarded for season 2011-12.”

The idea that the liability was potential and under discussion was then carried to RFC Interim Accounts dated 1st April 2011 where the liability was referred to under Exceptional item (note 1) £1,870. as

Note 1: The exceptional item reflects a provision for a potential tax liability in relation to a Discounted Option Scheme associated with player contributions between 1999 and 2003. A provision for interest of £0.9m has also been included within the interest charge.

In his covering statement Rangers Chairman Alistair Johnson said.

“The exceptional item reflects a provision for a potential tax liability in relation to a Discounted Option Scheme associated with player contributions between 1999 and 2003. Discussions are continuing with HMRC to establish a resolution to the assessments raised.”

Neither the Note nor covering statement nor the Grant Thornton letter are a true representation of the circumstances at 31st March 2011.

It was confirmed in the Craig Whyte court testimony that the liability was no longer potential at 31st March, Rangers having accepted on 21st March 2011 that they owed HMRC £2.8M. Any discussions thereafter were not about disputing the liability but agreeing terms to pay a back tax liability with its genesis in 2001. There was no dispute, but this misleading message of ongoing discussions was carried forward in the subsequent monitoring submissions made by RFC under Craig Whyte, after his takeover of RFC in May 2011, on 30th June (Art 66) and 30th September 2011. (Art 67).

When it emerged at the trial that the above justification for granting a licence was questionable, the SFA had no alternative but to instigate an investigation by their Compliance Officer, whose job it is understood is to gather together all relevant material and decide if there is a case to answer.

That case should not just focus on the part of RFC in this saga but also that of the SFA in terms of whether they used all their powers to first establish the true status of the liability, then did they cover up the truth when it became evident an overdue payable existed in August 2011 when Sherriff Officers called at Ibrox to collect the£2.8m overdue.

At time of writing on 25th October 2017 that SFA investigation is still underway and Celtic FC are waiting for the due SFA judicial process to run its course in order to be able to respond to Resolution 12 and shareholders.

In 2013 Celtic’s official response to the Resolution, based on what they were told by the SFA at the end of 2011, was that the Resolution was unnecessary.

If no acceptable explanation that clearly demonstrates that neither RFC nor the SFA have a case to answer emerges from the Compliance Officer investigation, pre-or post the AGM on 15th November 2017, then Celtic will have to decide if

a) they are going to stand by their initial stance that the Resolution is unnecessary or

b) pass Resolution 12 and take the matter to UEFA or

c) justify not doing so to their shareholders.

The club are keeping shareholder’s representatives in the picture as matters develop.

It should be noted with reference to the UEFA response from Andrea Traverso, Head of Club Licensing at UEFA to the shareholders representative’s lawyers in June 2016 that the five-year period to investigate had elapsed (due in no short measure to the SFA’s reluctance themselves to investigate in 2015) that during the Craig Whyte trial this was stated:

“In explaining the law on fraud generally, Mr Prentice Advocate Depute told the jury fraud involved a ” false pretense, dishonestly made in order to bring about some definite practical result” and suggested “it is not necessary that the result should be actual gain to the offender or loss to someone”.

This is a definition that would appear to apply to statements made by RFC in March/April 2011 and thereafter and there is no statute of limitations on investigation where corruption may have occurred, so option (b) is still open although there are other lesson learning reasons why UEFA should be involved.

UEFA Response of 8th June 2016 from Andrea Traverso, Head of UEFA Club Licensing.

For those interested in the details an account of Res12 lawyer’s activity with UEFA prior to and after the Traverso response can be viewed on line at https://drive.google.com/file/d/0B6uWzxhblAt9cFU2UVJyVlZXY1k/view?usp=sharing

GET BRENDAN RODGERS – THE ROAD TO PARADISE WITH A FREE GIFT INCLUDED FROM CQNBOOKSTORE.COM

Brendan Rodgers – The Road to Paradise is available now from CQNBookstore.com – the first 100 orders received will come with a free gift.

ORDER YOUR COPY NOW FROM CQNBOOKSTORE.COM AND RECEIVE A FREE GIFT WITH YOUR BOOK!

{kind=link}