FOR those interested in what the latest court ruling (Craig Whyte cleared of all charges) means for Res 12 and the wider debate about the running of Scottish Football and the competency of its own rules, procedures and personnel I invite you to take the time to participate in a little exercise.

It will be time-consuming but illuminating.

First, print off and read the detailed analysis of the evidence provided at the first tier tribunal of the Big Tax Case by Dr Heidi Poon. Forget her summation of the law, merely look at her recording of the evidence.

Secondly, read the report of Lord Nimmo Smith in detail and in particular focus on that part where he refers to the FTT decision and considers how he relies on that decision and his assessment of that evidence.

Thirdly, print off and read James Doleman’s twitter feed reporting on the evidence from the Craig Whyte trial.

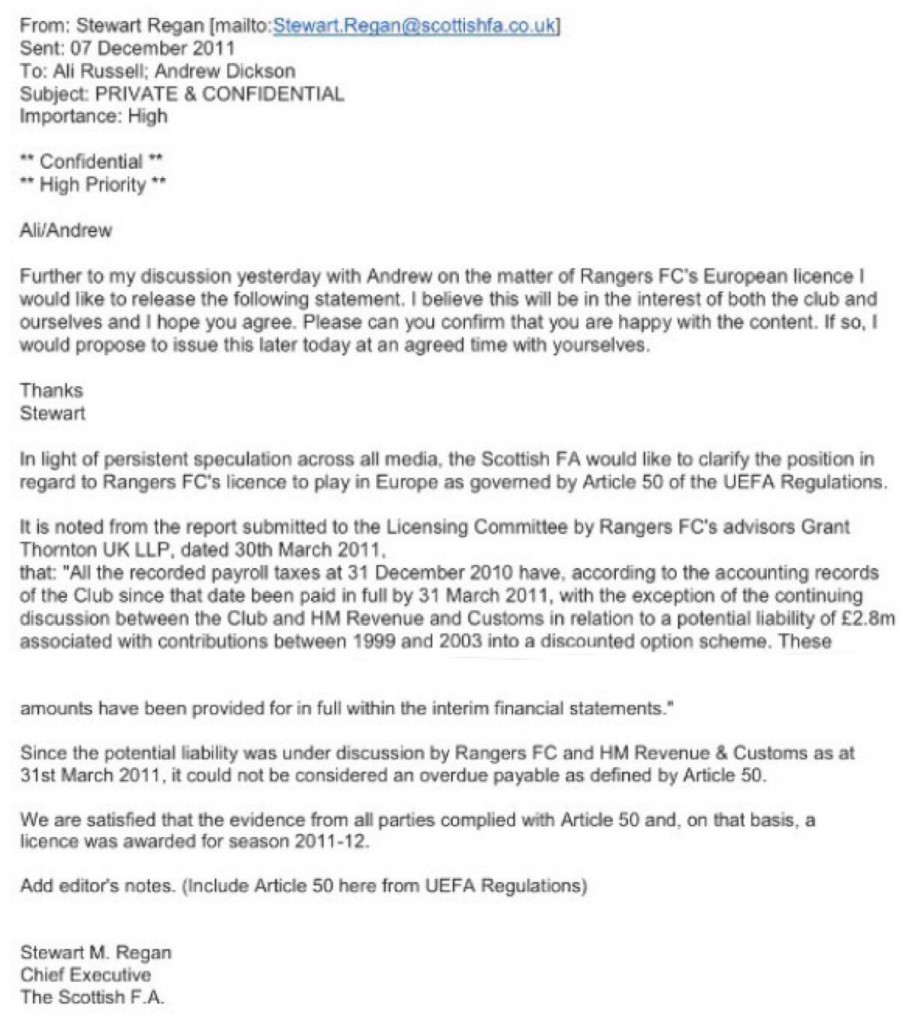

Fourth, stop and consider the previous statements issued by Stewart Regan re the granting and maintaining of the UEFA licence granted to Rangers in March 2011 (to be precise it was granted to Rangers on 18th April but based on circumstances pertaining as at 31st March and it was intimated to UEFA on 28th May 2011) and then the letter addressed to (Celtic) shareholders solicitors by Mr Traverso of UEFA.

Finally read the full decision and arguments presented to the Court of Arbitration for sport in the case of UEFA v FC Giannina.

There are many other documents I could refer you to but these will do for now.

Briefly, what can be taken from all of the above is as follows:

1. The details of football, tax and other rules are important and they are designed to bring about a system which makes the admnistration of football and tax affairs are uniform and fair.

2. Where those rules are not applied or conformed with (whether deliberately or by accident) then the rules fail, chaos follows, and prejudice and illegality results.

3. In the FTT it was clearly established that Rangers PLC and MIH deliberately witheld side letters from HMRC and that Mike McGill and Sir David Murray in particular lied to the appropriate tax authorities as to the existence of side letters which would have clearly scuppered the admitted tax avoidance scheme.

4. It has been repeatedly admitted that the same tax avoidance scheme was entered into for the purposes of securing the services of players which the club could not have otherwise afforded.

5, No other Scottish football club has ever participated this unlawful type of tax scheme nor stood accused of having their directors or officials lie to HMRC or any other official body.

6. It is now a matter of admission that an earlier tax avoidance scheme was wholly illegal and was instigated by the former Rangers employee and past SFA President Campbell Ogilvie.

7. It is a matter of admission that officials of Rangers PLC (a considerable number of whom are still involved in the current Rangers club) deliberately withheld side letters and other material information from the SFA and the then SPL for fear that disclosure of that information would result in (a) Rangers being found to have broken footballing rules and so sanctioned by the SFA and (b) Rangers being found to have breached tax laws and so found liable for past taxes.

It should be noted that despite their fear of sanction and the deliberate decision not to disclose for fear of sanction, Rangers continued to use the practices in question.

8. In the course of her FTT assessment of the evidence, Dr Poon is scathing in her assessment of the accuracy, reliability and veracity of the evidence provided by various Rangers personnel.

9. In the course of his cross examination in the Whyte trial, Donald Findlay was scathing in his assessment of the accuracy, reliability and veracity of the people in charge of Rangers at the time of the sale of the club to Whyte (late 2010 early 2011) and went so far as to question their business competence describing them as hopeless.

10. In the course of his summation to the jury (and later emphasised by Lady Stacey) Donald Findlay relied on internal memos from within MIH and Rangers PLC which showed that David Murray was hell bent on selling the club and was prepared to do whatever was needed to get the deal over the line.

This included failing to disclose the true finances of Rangers PLC in or around February/ March 2011 and a complete failure to disclose the existence of The Wee Tax Case and the accepted liability arising out of an accepted unlawful tax scheme as at February 2011.

Thus far, we have a clear practice of deliberately failing to disclose to HMRC, The SFA, The SPFL and Craig Whyte.

11. In the course of the trial it became apparent that David Murray was promised that if he sold Rangers and had the Rangers debt to the bank cleared in the process, he personally stood to gain from the repurchase of part of his metal business at a knock down price.

However, in a letter to Rangers Board Members David Murray not only failed to disclose any of this but specifically warranted that there was no such benefit accruing to him or MIH. Accordingly you can now add the directors of Rangers PLC to the list of people who have had material information witheld from them.

12. As part of the sworn testimony in court, it was accepted that the liability to HMRC was accepted by the club as being due as early as February 2011. That acceptance was binding on the club and it is clear that HMRC were treating the liability as overdue and were claiming tax and interest going back to 2001.

13. That liability was neither questioned or appealed by the seller or his advisers, but the interest charged was supposedly appealed by Craig Whyte and his advisers several months later. HMRC never treated the appeal as valid or timeous.

14. At various times, Stewart Regan has stated that at the material times, the wee tax case liability was either (a) not overdue or (b) was the subject of an extension of time agreed between RFC and HMRC and so did not breach UEFA licensing regulations.

HMRC have never accepted either of these propositions and it has previously been stated that when it comes to matters of disclosure, accuracy and truthfulness in relation to disclosure Rangers personnel have openly admitted they witheld the truth and failed to disclose the truth.

At no time have the SFA or the SPFL ever investigated the truth or accuracy of the submissions provided by Rangers PLC regarding the Wee Tax Case and both decided to deliberately remove all reference to these matters from the LNS enquiry.

15. In a letter to shareholders of Celtic PLC, the head of licensing at UEFA has stated that as at 28th May 2011 there was no reason for UEFA to suspect that there was any cause for concern in relation to the licence granted by the SFA to Rangers PLC.

16. It is unclear if UEFA have ever been informed that the board of Rangers PLC, and the owners of the club through MIH and its officers, have been repeatedly condemned and found guilty of repeated failure to disclose material items when making submissions or in answer to enquiries.

17. It is unclear whether or not UEFA were made aware of the fact that officials of Rangers PLC accepted there was a tax liability outstanding in February 2011 and which remained outstanding as at 31st March 2011, nor is it clear if they were made aware of the fact that this liability was not openly disclosed to the eventual buyer of the club and was witheld from him at the material time.

18. Stewart Regan of the SFA is on record as stating that having awarded a UEFA licence to Rangers in or around March/April 2011, all subsequent procedures regarding UEFA compliance had nothing to do with the SFA and were for UEFA to deal with.

19. In his letter to Celtic shareholders, Mr Traverso contradicts 18 above quite clearly.

20. When writing to the Chief Executive of Celtic Football Club, Stewart Regan states clearly that the procedures and processes adopted by the SFA in relation to the grant and award of UEFA licences during the course of 2011 was subject to UEFA audit with the result that UEFA stated they were more than satisfied with the SFA processes.

Official UEFA reports state that the SFA was not audited at all during season 2010/2011 or season 2011/2012 in relation to licensing processes.

21. While Stewart Regan has maintained that the SFA played no part in monitoring compliance with UEFA licences, Mr Traverso of UEFA has stated in writing that not only were the SFA monitoring compliance in 2011 but were contemporaneously monitoring events for season 2012/2013. Both statements cannot be correct.

22. Mr Traverso from UEFA has stated that during the course of season 2011/2012, UEFA were advised by the SFA (at some unspecified point and for reasons which have never been disclosed) that Rangers PLC no longer complied with UEFA licensing provisions.

23. The facts stated at 22 above were not disclosed to the Chief Executive of Celtic PLC in any correspondence between Celtic and the SFA, and the Chief Executive of the SFA would appear not to have disclosed that they informed UEFA that Rangers PLC no longer complied with licensing provisions nor why the SFA reached that conclusion.

24. It is plain from the testimony at the High Court and elsewhere that it was essential in 2011/2012 for Rangers to gain financially from European competition failing which administration (which had been discussed by the board in 2010) was inevitable.

25. From February 2011 onwards the HMRC position that the Wee Tax Case was overdue remained consistent and it never changed. No money was ever paid to this liability and it was clearly accepted as being due in the Share Sale and Purchase Agreement signed between Murray and Whyte dated 6th May some three weeks before the award of the licence was submitted to UEFA with a condition being added that Whyte would undertake to make payment of the sum due.

26. No payments of the sums referred to in the Share Sale and Purchase Agreement were made as at 30th June or 30th September both of which are key dates in the UEFA monitoring processes.

27. Despite all of the above, Rangers PLC draft and provisional accounts continued to refer to the Wee Tax Case Liability as a “potential” liability and former Rangers PLC Chairman Alistair Johnston repeated the mantra that the liability was potential despite fellow board members agreeing with HMRC that the sums were actually due.

28. In the case of UEFA v FC Giannina the court determined that when a company board accepted that a tax liability was due in writing then it was immediately due and or overdue irrespective of the technicalities of national legislation or any other documents. This would then mean that the Wee Tax Case liability was automatically accepted as at February 2011 and was overdue.

29. In the case of Uefa v FC Giannina – the stated UEFA position is that when any club fails to disclose material information in any application for a licence or in support of an application for a licence or in any set of financial accounts required to support an application for a licence, then the failure to disclose and the submission of inaccurate accounts and information will immediately make that application or the accounts concerned null and void and as if no application had ever been received at all with there being no need for UEFA to investigate each and every circumstance or potantially serious breach of the rules.

In other words if you seek to cover up any dishonesty or any failure to comply then the application is automatically rejected for that year and for every year that a club failed to disclose.

30. FC Giannina failed to disclose that they had side letters and contracts with their players, failed to disclose their full wages to the Greek FA, failed to pay all their taxes on the sums due to the players as a result of payments made to those players, failed to properly disclose the true nature of sums outstanding to the tax authorities in Greece, attempted to deceive the Greek FA by not disclosing the whole truth re the position with the Greek Tax authorities and had the UEFA licence initially awarded to them by the Greek FA in season 2011/12 withdrawn within a matter of months. They were then banned from European competition for a period of time.

31. At no time have the SFA ever commented on the impact of the case against FC Giannina in relation to the Wee Tax Case or the Big Tax Case, nor the findings of the SPFL enquiry which ruled that Rangers PLC had deliberately failed to disclose certain material matters and that the registration of players was technically correct but incomplete in material terms (Giannina would suggest that this is the wromg approach) nor a previous finding during which the panel described the actions of the then Rangers board as being “as close to match fixing as you can possibly get” or words to that effect.

Finally, I would add that Stewart Regan’s pronouncement yesterday that the SFA would take legal advice about chasing a man who has previously been made bankrupt for an unpaid £200k liability ranks as one of the most obvious squirrells in the history of PR.

Regrettably, the MSM in Scotland failed to ask him how a bankupt could ever be forced to pay a debt having been declared bankrupt in the interim and so appear to have swallowed the squirrel hook line and tail!

No one has botherd to ask them if they will be reviewing their own procedures and the submissions made to the SFA by what Jack Irvine described as a Rangers board which was a “snake pit of rumour, innuendo, lies, intimidation, fraud, corruption and these are just the good points”.

The full quote from Irvine, describing the outgoing board headed by Alistair Johnston which made the application for the UEFA licence in Mrach 2011 reads as follows:

“The events of the last couple of days will by now have convinced you that the business side of [the]Glasgow-based football club is a snake pit of rumour, innuendo, lies, intimidation, fraud, corruption and these are just the good points.”

When read in conjunction with the observations of Dr Poon it is an assessment which is hard to disagree with.

At the time concerned the business side of Rangers was run by inter alia Dave King, Alistair Johnston, Paul Murray, Andrew Dickson and others.

It should be rememberd that when the Chief Executive of Celtic Football Club wrote to the SFA Chief Executive about SFA practices and procedures, the SFA Chief Executive drafted a reply and sent his draft to Ibrox for comment before releasing a final response to Celtic.

The SFA Chief Executive’s draft reply was rejected by the then powers that be at Ibrox on the grounds that the reply could raise questions which would be “Embarassing for both of us!”

Written by BRTH for the Res12 Campaign.

{kind=link}